Blood Collection Market Outlook: Diagnostic Testing Demand and Healthcare Expansion Opportunities

The blood collection market is experiencing steady growth, driven by increasing demand for diagnostic testing, rising prevalence of chronic diseases, and expanding healthcare infrastructure worldwide.

According to IMARC Group's latest research publication, The global blood collection market size was valued at USD 7.26 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 10.36 Billion by 2033, exhibiting a CAGR of 4.03% during 2025-2033.

How AI is Reshaping the Future of Blood Collection Market

- Automated Vein Recognition and Robotic Phlebotomy: AI-powered systems use computer vision with ultrasound imaging to precisely locate veins, achieving 95% first-needle accuracy. Intelligent robots like MagicNurse and Aixam Divine Needle have completed thousands of successful punctures, reducing clinician workload while enhancing patient comfort and procedural consistency.

- Predictive Donor Management and Scheduling Optimization: Machine learning analyzes historical donation patterns and regional demand to optimize blood bank scheduling and retention strategies. These intelligent systems ensure reliable supply management while improving donor experiences through personalized communication and convenient appointment scheduling based on availability predictions.

- Quality Control Through Automated Sample Analysis: AI algorithms monitor sample quality by detecting hemolysis, clotting issues, and fill volume deviations in real-time. Automated systems assess serum indices and specimen integrity, preventing substandard samples from entering diagnostic workflows and reducing costly redraws while maintaining laboratory accuracy.

Blood Collection Industry Overview:

The chronic disease epidemic is fundamentally reshaping blood collection demand, with 129 million Americans experiencing one or more major chronic conditions—42% managing two or more simultaneously. These conditions account for 90% of the USD 4.1 trillion annual U.S. healthcare expenditure, driving unprecedented testing volumes. The International Diabetes Federation reports 589 million adults worldwide living with diabetes, projected to reach 853 million by 2050, creating sustained diagnostic equipment demand. North America dominates with 41.2% market share, supported by advanced infrastructure and regulatory frameworks including the FDA's Quality Management System Regulation aligning with ISO 13485:2016, streamlining device clearances and encouraging domestic manufacturing investments.

Blood Collection Market Trends & Drivers:

Automated and robotic blood collection systems are revolutionizing traditional phlebotomy practices across clinical settings. Terumo's Reveos automated whole blood processing system—the first FDA-approved device of its kind in the U.S.—reduces processing steps from 26 to just 9, dramatically improving laboratory efficiency. Vitestro's Aletta autonomous robotic phlebotomy device received CE marking, enabling European deployment for high-volume collection sites processing 100+ patients daily. BD launched the MiniDraw Capillary Blood Collection System integrating Babson's BetterWay technologies, enabling comprehensive test results from just six drops of finger-collected blood. These innovations address persistent phlebotomist shortages while delivering consistent quality and reducing needlestick injuries—BD's UltraTouch collection set reportedly decreases needle injury risk by 88%. The shift toward automation extends beyond hospitals, with point-of-care devices enabling home-based testing for chronic disease management and decentralized clinical trials.

Point-of-care and home-based diagnostic solutions are expanding blood collection accessibility beyond traditional clinical environments. The COVID-19 pandemic accelerated adoption of portable self-collection devices, with patients increasingly demanding convenient testing options. Tasso partnered with Lindus Health to deploy remote blood collection systems for clinical trials, increasing patient accessibility while reducing procedure discomfort. Self-microsampling technologies using adhesive-activated devices enable collection volumes between 0.1-0.5 mL through painless skin punctures, with patients reporting greater convenience compared to traditional finger-pricking methods. Greiner Bio-One introduced Vacuette Z-Grip PLUS vacuum tubes with enhanced ergonomics for improved handling in both clinical and home settings. The capillary blood collection segment is experiencing rapid growth driven by minimally invasive approaches ideal for glucose monitoring, cholesterol testing, and rapid diagnostics—applications perfectly suited for telehealth expansion and remote patient monitoring programs serving aging populations and chronic disease patients requiring frequent testing.

Strategic manufacturing investments and technological partnerships are strengthening global supply chains and accelerating innovation. BD committed USD 2.5 billion to U.S. capacity expansion, including USD 30 million investment in its Sumter facility producing billions of Vacutainer blood collection products annually—celebrating 55 years of operation supporting diagnostics, treatment, and medical research. Terumo invested USD 15 million localizing Trima Accel and Spectra Optia production in China, responding to Asia-Pacific's projected 7.28% growth rate driven by "Healthy China 2030" initiatives and India's expanding laboratory networks. Terumo and Roche formed a strategic partnership combining medical device expertise with diagnostic capabilities to co-develop next-generation venous collection systems. NAMSA partnered with Terumo on regulatory approval and commercialization services, streamlining global market access. Streck launched Protein Plus BCT for stabilizing plasma proteins at room temperature, while QIAGEN introduced the QIAseq Multimodal DNA/RNA Library Kit simplifying genetic library preparation from single blood samples—innovations expanding research applications and diagnostic precision.

Leading Companies Operating in the Global Blood Collection Industry:

- Becton, Dickinson and Company

- Terumo Corporation

- Greiner Bio-One International GmbH

- SARSTEDT AG & Co. KG

- Nipro Medical Corporation

- Fresenius Kabi AG

- Haemonetics Corporation

- F.L. Medical S.r.l.

- Improve Medical Instruments Co., Ltd.

- Sekisui Medical Co., Ltd.

- Cardinal Health

- McKesson Corporation

Blood Collection Market Report Segmentation:

By Product:

- Needles and Syringes

- Blood Collection Tubes

- Blood Bags

- Others

Needles and syringes represent the largest segment, holding 29.2% market share, driven by their widespread application across routine blood draws, transfusions, and diagnostic procedures.

By Application:

- Diagnostics

- Treatment

Diagnostics dominates with 66.7% market share, propelled by rising chronic disease prevalence requiring frequent blood testing for conditions including diabetes, cardiovascular disorders, and cancer.

By End Use:

- Hospitals

- Diagnostics Centers

- Blood Banks

- Others

Hospitals lead with 37.2% market share, supported by high procedural volumes spanning emergency care, surgical interventions, and comprehensive patient monitoring requiring consistent blood supply.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America exhibits clear market dominance with 41.2% share, supported by advanced healthcare infrastructure, substantial R&D investments, and established clinical diagnostics ecosystems.

Recent News and Developments in Blood Collection Market

- January 2025: Becton, Dickinson and Company introduced an advanced blood collection tube line enhancing sample stability by 15% compared to previous models, reducing the need for patient redraws and improving diagnostic workflow efficiency across clinical laboratories.

- January 2025: Terumo BCT signed a strategic Memorandum of Understanding with Shandong Institute of Medical Devices and Pharmaceutical Packaging Inspection, strengthening technical research and innovation capabilities focused on blood component collection and processing technologies.

- December 2024: BD and Babson Diagnostics launched the BD MiniDraw Capillary Blood Collection System incorporating BetterWay technologies, enabling comprehensive test results from as few as six finger-collected blood drops for improved patient comfort.

- April 2025: Greiner Bio-One obtained regulatory approval for Vacuette Z-Grip PLUS vacuum blood collection tubes featuring improved ergonomics and handling characteristics, optimizing laboratory workflow and phlebotomist efficiency in diagnostic settings.

- March 2024: Terumo Corporation entered a strategic partnership with F. Hoffmann-La Roche to co-develop next-generation venous blood collection devices, combining Terumo's medical device engineering expertise with Roche's diagnostic technology capabilities.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

James Whitman

With years of experience in analyzing global industries, I specialize in delivering actionable market insights that help businesses stay ahead in an ever-changing landscape.

Keep reading

More stories from James Whitman and writers in Futurism and other communities.

Wireless Sensors Market Outlook: IoT Integration and Smart Monitoring Growth Opportunities

According to IMARC Group's latest research publication, The global wireless sensors market size was valued at USD 16.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 56.1 Billion by 2034, exhibiting a CAGR of 14.44% from 2026-2034.

By James Whitman8 days ago in Futurism

The Fears of AI And How Much Fun It Can Be

ChatGPT has come a long way, as has AI in general. There are those people who are scared of it, and for understandable reasons. People fear that as technologies advance, they’ll be replaced in the workforce. Then, there are the fears that AI could evolve into something that brings us to the brink of extinction.

By The Man Behind The Maskabout 20 hours ago in Futurism

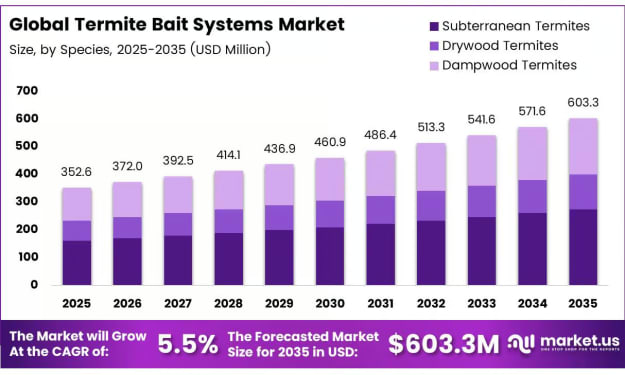

Termite Bait Systems Market Report: USD 603.3 Million by 2035 at 5.5% CAGR

Market Overview The Global Termite Bait Systems Market is projected to grow from USD 352.6 million in 2025 to USD 603.3 million by 2035, registering a CAGR of 5.5% during the forecast period from 2026 to 2035.

By Hayden Kulasabout 6 hours ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.