Automotive Aluminium Market Insights: Structural Components, Fuel Economy & Forecast to 2034

How advancements in aluminium processing, structural applications, and fuel efficiency improvements are transforming the automotive aluminium market

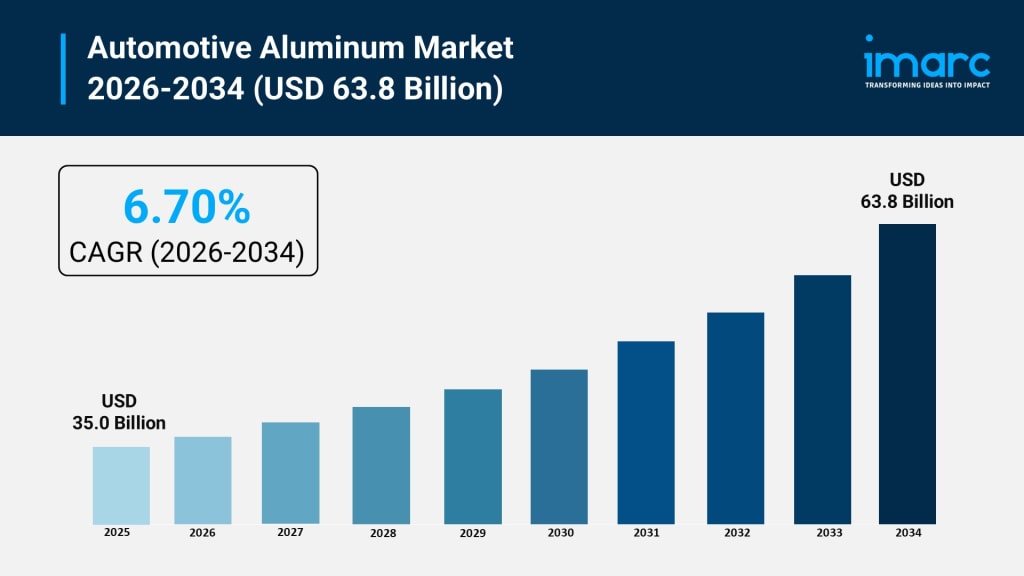

Rising demand for lightweight vehicles, rapid electric vehicle (EV) adoption, and increasingly stringent emission regulations are reshaping how automakers think about material choices — and aluminium is right at the center of that shift. According to IMARC Group’s latest data, the global automotive aluminium market size was valued at USD 35.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 63.8 Billion by 2034, exhibiting a CAGR of 6.70% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 40% in 2025. The region benefits from extensive vehicle manufacturing infrastructure, strong government support for electric vehicle adoption, and rising demand for lightweight materials driven by stringent emission regulations and growing consumer preference for fuel-efficient automobiles, all contributing to the automotive aluminium market share.

Automotive aluminium has moved well beyond a niche application — it’s now a foundational material across passenger cars, commercial vehicles, and electric platforms worldwide. The core appeal is straightforward: aluminium is roughly one-third the weight of steel yet delivers comparable strength, which translates directly into better fuel economy, lower emissions, and greater EV range. As regulators tighten CO₂ standards across the EU, the US, China, and India, automakers are under real pressure to cut vehicle weight, and aluminium is one of the most proven tools available. Add in its recyclability — up to 95% of automotive aluminium can be reused — and it’s clear why the material sits at the intersection of performance, compliance, and sustainability. Key growth segments include body structures, powertrains, suspension systems, and battery enclosures for EVs, with cast, rolled, and extruded forms each playing distinct roles across different vehicle types and weight targets.

Request a Business Sample Report for Procurement & Investment Evaluation

Automotive Aluminium Market Growth Drivers:

Stringent Emission Regulations and Fuel Efficiency Mandates

Governments across major auto markets are pushing hard on emissions. The EU’s target to cut new car CO₂ emissions by 55% by 2030 and the US EPA’s updated CAFE standards are forcing OEMs to make structural weight reductions across their lineups. Aluminium is the go-to solution. According to the Aluminum Association, aluminium content per vehicle is set to grow to around 550 pounds by 2030 — up from 165 pounds in 1990. Replacing one kilogram of steel with aluminium can cut lifetime CO₂ emissions by approximately 19 kilograms per vehicle, making it a practical, measurable way for manufacturers to hit regulatory targets without sacrificing performance or safety.

Surging Electric Vehicle Production

The EV revolution is one of the most powerful demand catalysts for automotive aluminium. Because battery packs add significant mass, automakers turn to aluminium to offset that weight and preserve driving range. Global EV production exceeded 14.2 million units in the past year, with over 82% of those vehicles incorporating aluminium alloy components. Each electric vehicle requires approximately 260 kg of aluminium on average. Battery trays made from aluminium alone deliver weight savings of around 22 kg per vehicle. Companies like Jaguar Land Rover have already locked in dedicated supply agreements for aluminium-intensive EV platforms, signalling that this is now a core material strategy, not an optional upgrade.

Growing Preference for Recyclable and Sustainable Materials

Sustainability pressures from consumers, investors, and regulators are pushing automakers to rethink material sourcing from the ground up. Aluminium fits this agenda well. According to the International Aluminium Institute, around 90% of the aluminium used in vehicles is recycled at end-of-life, and reprocessing it requires only 5% of the energy needed to produce primary aluminium. Novelis, one of the leading aluminium suppliers to the auto sector, reported achieving 63% average recycled content across its portfolio through closed-loop partnerships with carmakers. The European transport sector already accounts for 42% of total semi-fabricated aluminium demand, with sustainability commitments from OEMs like BMW and Ford accelerating adoption of low-carbon aluminium sourcing across their supply chains.

Automotive Aluminium Market Trends:

Rise of Mega-Casting and Advanced Manufacturing Techniques

One of the more transformative shifts in automotive manufacturing is the move toward large-scale aluminium casting — producing entire vehicle underbody sections as a single piece rather than assembling dozens of welded components. This approach, widely associated with Tesla’s Gigacasting technology, is gaining traction across the industry. In April 2025, PWO launched an aluminium hybrid casting process that cuts vehicle weight by up to 20%, already adopted by a German luxury automaker for its 2026 lineup. Toyota has announced plans to incorporate Gigacasting into a 2026 EV model as part of its ambition to produce 1 million EVs annually by 2027. These processes cut production time and improve structural consistency at scale.

Expansion of High-Strength Alloy Development for EVs

Automakers need aluminium that does more than just reduce weight — they need alloys engineered specifically for the structural and thermal demands of EV architecture. Between 2023 and 2024, more than 15 new high-performance aluminium alloy grades designed for electric vehicles were introduced globally. UACJ Corporation introduced next-generation alloys optimised for EV battery casings in early 2026, while Alcoa launched its A210 ExtruStrong, a 6000-series high-strength alloy targeting lightweight structural applications. Novelis also launched advanced high-strength alloys for EV platforms in February 2026. Alloy content in hybrid vehicle platforms alone grew by 6.1% in 2024, showing that material innovation is actively tracking the pace of vehicle electrification.

Capacity Expansion and Strategic Supply Chain Investment

Suppliers are investing heavily to keep pace with surging automotive aluminium demand. In January 2025, Jindal Aluminium expanded its automotive-grade aluminium extrusion capacity by 30% to serve growing EV demand from Indian and Southeast Asian manufacturers, pairing the expansion with a dedicated R&D centre for high-strength alloys. In March 2026, Alcoa extended its rolling and extrusion capacity to meet aerospace and automotive demand, while Constellium opened a new facility for automotive aluminium sheet specifically targeting EV structural components. Hydro committed a EUR 29 million investment in a new extrusion press in Denmark. India’s PM E-Drive scheme, which allocated USD 520 million to electric bus procurement, is also pulling aluminium demand upward through government-backed EV infrastructure.

Recent News and Developments in Automotive Aluminium Market

March 2026: Alcoa Corporation expanded its rolling and extrusion capacity to address growing demand across the automotive and aerospace sectors, reinforcing its position as a key supplier for lightweight vehicle platforms globally.

February 2026: Novelis launched a new range of advanced high-strength aluminium alloys targeting lightweight EV and commercial vehicle applications, continuing its push to grow recycled content across its automotive supply partnerships.

January 2026: Aluminium Corporation of China (Chinalco) and Rio Tinto agreed to acquire a controlling stake in Companhia Brasileira de Aluminio for approximately USD 904 million, expanding their combined global footprint and raw material access.

January 2025: Jindal Aluminium Ltd. expanded automotive-grade aluminium extrusion capacity by 30% to meet rising demand from Indian and Southeast Asian EV manufacturers, while also launching a dedicated R&D centre for high-strength alloy development.

April 2025: PWO launched an innovative aluminium hybrid casting process for lightweight chassis components, achieving weight reductions of up to 20%. The technology has been adopted by a German luxury automaker for its 2026 vehicle models.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

Suhaira Yusuf

I specialize in Consumer Insights, focusing on transforming detailed market data into strategic business solutions that accelerate growth and improve customer engagement.

Keep reading

More stories from Suhaira Yusuf and writers in Futurism and other communities.

Docking Station Market Growth: Multi-Device Integration, Productivity Tools & Forecast to 2034

The humble docking station has quietly become one of the most essential pieces of hardware in the modern workplace. As laptops replace desktops and hybrid work becomes the norm rather than the exception, the need to instantly transform a portable device into a full workstation has never been greater. According to IMARC Group’s latest research, the global docking station market size reached USD 8.2 Billion in 2025. Looking ahead, IMARC Group projects the market to reach USD 11.7 Billion by 2034, exhibiting a growth rate (CAGR) of 3.84% during 2026–2034. North America currently dominates the market, holding a market share of over 42.4% in 2025, fuelled by high laptop penetration, strong enterprise IT spending, and a well-established culture of flexible work.

By Suhaira Yusuf6 days ago in Futurism

The Fears of AI And How Much Fun It Can Be

ChatGPT has come a long way, as has AI in general. There are those people who are scared of it, and for understandable reasons. People fear that as technologies advance, they’ll be replaced in the workforce. Then, there are the fears that AI could evolve into something that brings us to the brink of extinction.

By The Man Behind The Maskabout 19 hours ago in Futurism

GCC Soundbar Market Growth: Role of E-Commerce & Omni-Channel Retail Strategies

According to IMARC Group's latest research publication, the GCC soundbar market size reached USD 114.7 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 223.2 Million by 2034, exhibiting a growth rate (CAGR) of 7.45% during 2026-2034.

By Abhay Rajput4 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.