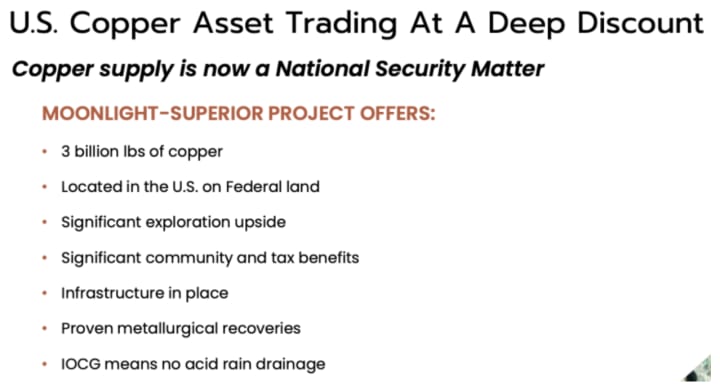

US Copper Corp, 3 Billion + pounds in the USA

Last month US Copper shares soared to C$0.415, but have fallen to C$0.15. High risk for sure, but buying opportunity?

Near-month copper (“Cu“) futures hit a record ~$14,525/tonne (US$6.58/lb.) in January but have fallen to ~$5.45/lb. in large part due to the Middle East situation. However, I believe the long-term narrative for Cu demand is intact.

And, sustainable supply to Western nations remains challenged. Freeport’s Grasberg in Indonesia — the world’s 2nd largest Cu mine — declared force majeure after a major mudslide; its main pit (70% of output) won’t fully recover until next year.

China’s top smelters agreed to cut production by > 10% in 2026. Ivanhoe Mines’ Kamoa-Kakula in the DRC lowered 2026 guidance by a third after flooding depleted its stockpiles. Teck Resources’ Quebrada Blanca slashed 2026 guidance by 26%.

By far the largest Cu producing country Chile has seen average mined Cu grades fall from ~1.1% in 2006 to ~0.6% today. The world’s easy Cu has been found, and much of it has been exploited.

Readers are reminded that among the top dozen Cu producing countries, fully half China, Russia, the DRC, Indonesia, Zambia & Kazakhstan are difficult or very difficult for the West to rely upon. Yet, demand remains as strong as ever.

War is forcing nations to beef up their militaries, and replenish munitions & equipment. Modern warfare is Cu-intensive. Every artillery shell, missile, aircraft, ship, armored vehicle & communications system relies on Cu for casings, wiring, electronics & motors.

Precision-guided munitions, radar systems, and field communications are all highly Cu-dependent. Military base & logistics infrastructure amplifies demand. And of course, rebuilding war-torn cities requires copious amounts of Cu.

Copper is shifting from a cyclical +2.5% (GDP-like) growth rate base metal to a critical infrastructure bottleneck metal that could experience periods of 4%/yr expansion. Mined Cu deficits are unavoidable for several years, possibly a decade.

Only increased recycling and/or new mining technology can save the day, and they will to some extent, but it won’t stop the Cu price from rising to meaningfully higher levels.

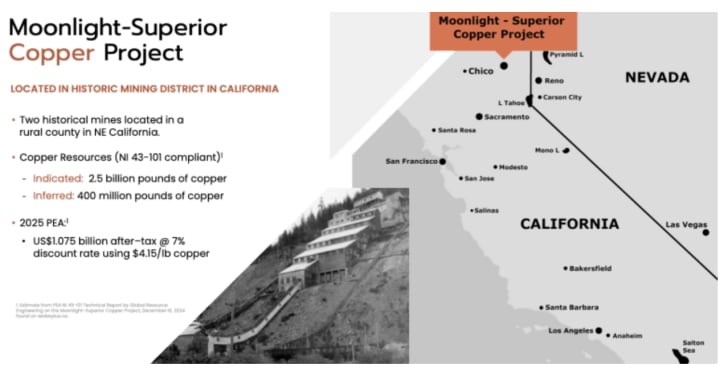

Given geopolitical events, I believe the U.S. & Canada are two of the best places on earth to develop Cu projects. A company I continue to like is US Copper Corp., a storied past-producer, with its flagship 100%-owned 6,056 acre Moonlight-Superior project in NE California, USA.

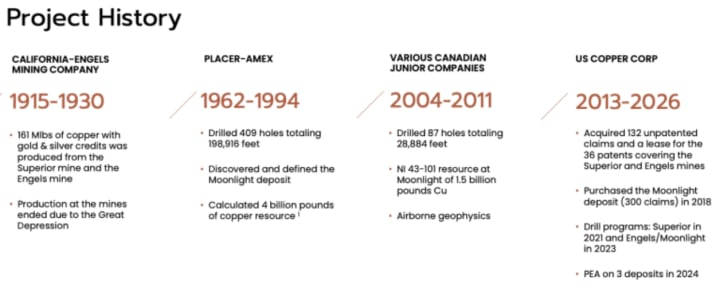

US Copper acquired the claims/patents covering the past-producing Superior & Engels mines out of bankruptcy in 2013. In 2016, it optioned the Moonlight claims, then acquired the claims outright in 2018.

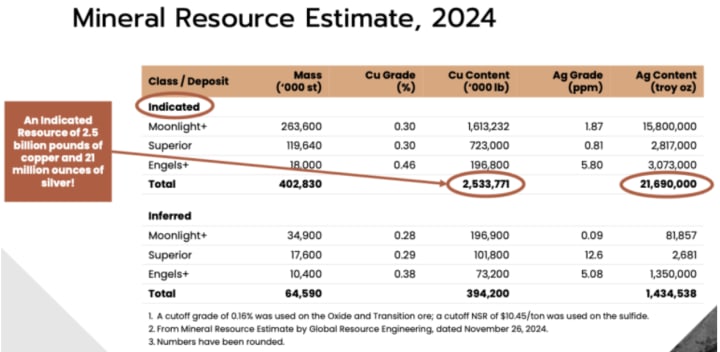

There are dozens of interesting Cu projects in the U.S. Yet, how many have over 3 billion Cu Eq. pounds (Indicated + Inferred)? Not many. Moonlight also has an estimated 23.1M ounces of silver (“Ag“), not an insignificant amount. Cu is now deemed a critical material in most parts of the world.

The Company has delivered a robust PEA using $4.15/lb. Cu., 24% below the current $5.45/lb.At $4.15, the post-tax NPV(7%) was ~C$1.5B, and at $5.45/lb. it’s ~C$2.6B. Compare that to the Company’s enterprise value of just ~C$21M (C$0.15/shr.).

Note: Moonlight’s 0.31% Cu grade is low compared to S. American mines/projects, but in B.C. Canada Teck Resources mines 0.25-0.28% Cu, Hudbay Minerals ~0.24%, and Taseko Mines ~0.23%. In Arizona, Freeport McMoRan operates at 0.20-0.35% Cu., and Rio Tinto is earning into a project in Nevada with a grade of 0.18% Cu Eq.

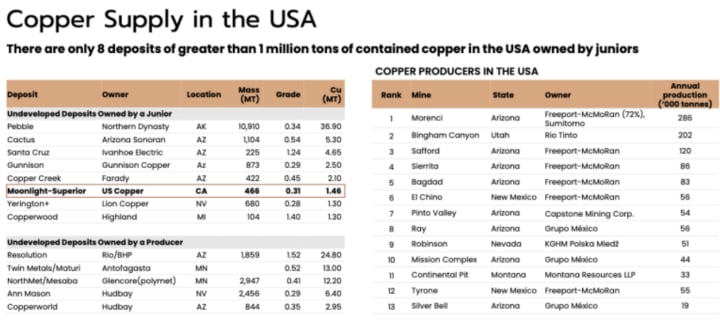

Two interesting juniors in the table, Gunnison (backed byRio Tinto) & Faraday (Lundin Group), have an average market cap of ~C$600M. US Copper is valued at less than 5% of that.

Are these projects more advanced than US Copper’s Moonlight? No, both are at PEA-stage. Ivanhoe Electric is backed by Cu mining legend Robert Friedland, the most important (and impressive) Cu pundit on earth, and major Saudi Arabian mining company Ma’aden.

HudBay just acquired Arizona Sonoran for its large, high-grade, PFS-stage project, paying ~C$0.13/lb.By contrast, US Copper is valued at ~C$0.008/lb., just 1/16 that of the Arizona Sonoran deal. Lion Copper’s market cap is C$165M, it too is backed by Rio.

Highland Copper is meaningfully supported by Orion Mine Finance & Osisko Gold Royalties. It’s valued at ~C$90M.

Other giant & large players in the western U.S. include; BHP, Freeport McMoran, Antofagasta plc, Glencore, Grupo Mexico/Southern Copper, Sumitomo, Mitsui, Mitsubishi Corp., Marubeni Corp. ITOCHU Corp., KGHM Polska, and Capstone Mining.

Readers are reminded that Newmont & Barrick Mining now have very substantial copper endowments, and royalty companies like Wheaton Precious Metals, Franco-Nevada & Royal Gold have mostly precious, (but growing Cu exposure) via deals with juniors in the U.S.

What’s my point in named-dropping so many companies? How many juniors have 3 billion plus pound Cu Eq. resources in the U.S. WITH NO STRATEGIC BACKING (yet)?!?

Although it might be 2027 before US Copper secures a partner, I see no reason for it not happening. Most of the players listed above in red are well aware of US Copper’s Moonlight-Superior.

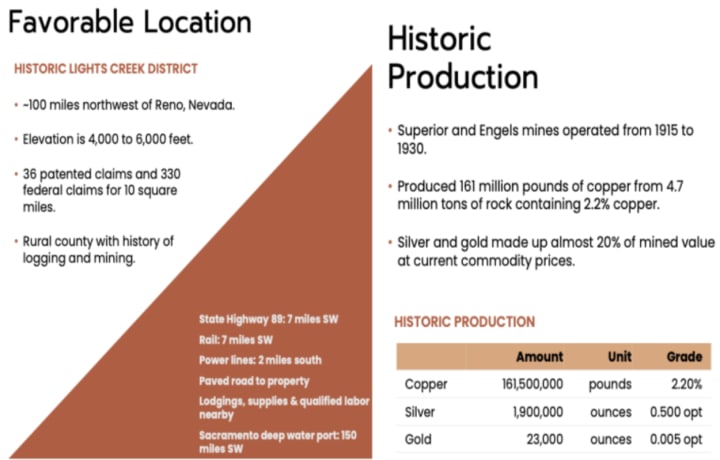

Moonlight is well located ~100 miles NW of Reno, Nevada. There’s ample regional infrastructure in place. The Project is comprised of 36 patented claims + 330 federal claims over 10 sq. miles.

It’s in a rural county with a long history of logging & mining. Therefore, local support is considered to be positive. State Highway 89 and a rail connection are both within 7 miles, and a power line is 2 miles away. A deep water port in Sacramento is 150 miles to the SW.

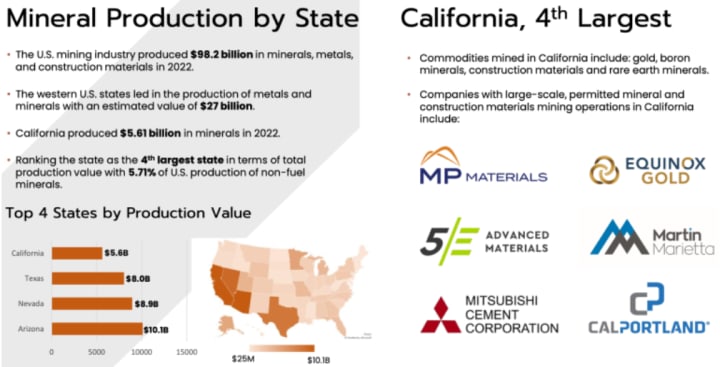

Many readers have questions about the ability of California mining projects to get permits & approvals. Certain counties and a few case-specific situations (dating back many years) showcased meaningful challenges (long delays or rejections).

However, in the past few years things have changed for the better, and the current U.S. Administration is the most favorable for California and for the entire country in decades. To be clear, Moonlight is on Federal lands, a very good thing given the current Administration.

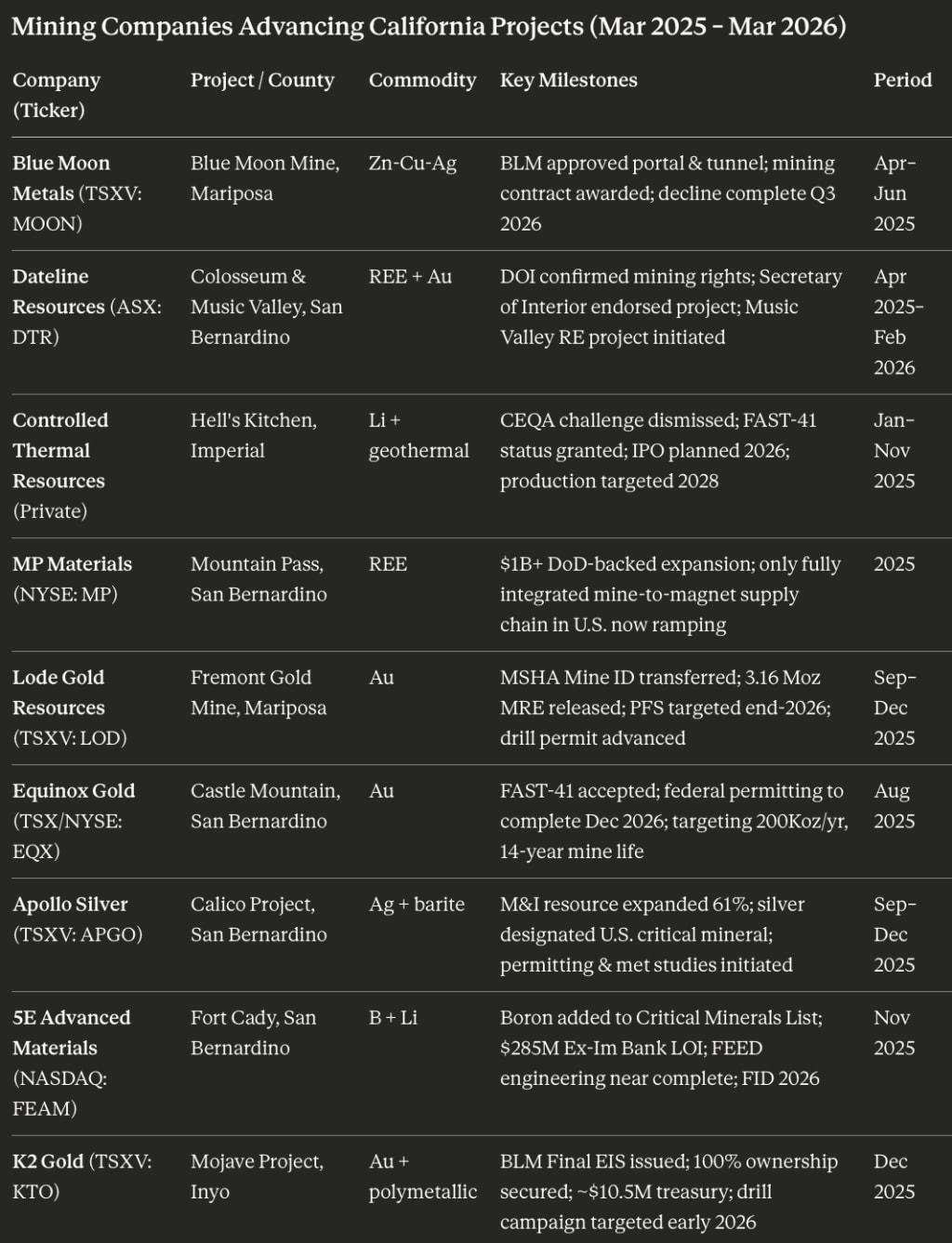

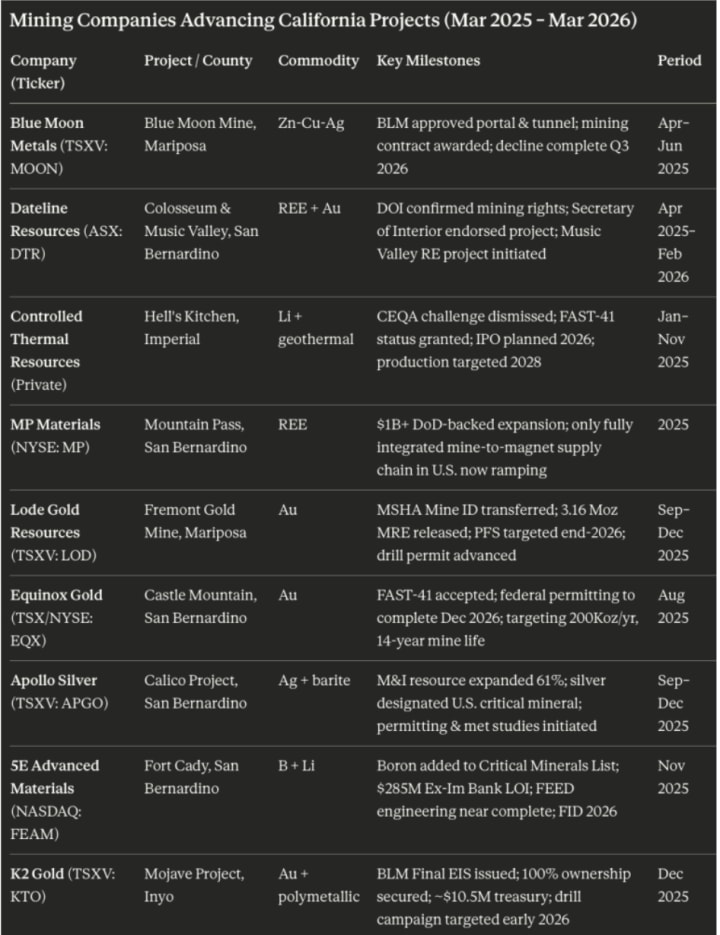

Take a look at this table… California is open for metals/mining…

The following table shows numerous companies, (explorers, developers & producers) with gold, silver, copper, zinc, lithium, REE assets in California that have made good progress in the State in the past year. This doesn’t include oil/gas or cement/aggregates companies.

At some point, investors will recognize that very significant geopolitical, safety/security, local opposition & water concerns around the world make projects in California not so bad on a relative basis!

Earlier this year In Mexico there was a deadly kidnapping at a world-class silver project. In S. America local opposition (in select regions in certain countries) is a serious risk factor. Water scarcity is a major challenge, leading to logistical & cost problems.

Geopolitically, the West vs. China/Russia/Iran has taken a horrible turn, with no (clear) end in sight. Being largely shut out of N. America, China’s buying all the assets it can across Africa & S. America. To say US Copper is ideally positioned in the USA is a gross understatement.

In my view, if Moonlight were 50-60 miles to the east, in Nevada, or in Arizona instead of California, it might be valued A LOT higher… But, therein lies the potential for a re-rate in the coming months.

Note, shares recently surged to C$0.415 on extraordinary trading volume, but have settled back to C$0.15. Over 34M shares (combined in the U.S. & Canada) traded on Feb. 24th alone. Presumably, someone wanted in badly… Management has no comment on this topic.

Importantly, management does NOT need to raise cash, it has enough to last the remainder of the year.

To reiterate, the world is an increasingly dangerous & uncertain place! Risks are everywhere, many can’t be avoided. In my opinion, the RELATIVE risk of California (permitting) to all other known + unknown risks globally, is low.

US Copper offers a compelling risk/reward proposition –> 3 billion+ Cu Eq. pounds in the USA valued at less than 2% of its post-tax NPV(7%)(at spot pricing).

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about US Copper, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of US Copper are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, US Copper was an advertiser on [ER] and Peter Epstein owned no shares in the company, but may acquire shares in the open market in the near future.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

About the Creator

Keep reading

More stories from writers in Trader and other communities.

bitcoin usd guide: How to Spot Winning Moves in the Market

Understanding bitcoin usd is becoming essential for anyone interested in growing their money. The value of Bitcoin in US dollars changes every day, sometimes dramatically. By learning the patterns and secrets behind bitcoin usd, investors can make smarter choices and take advantage of opportunities as they appear. For beginners looking to start safely, check our guide on how to invest in Bitcoin for beginners.

By John.doe7985 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.