Global Prostate Cancer Diagnostics Market Set to Surge: Early Detection and Innovation Drive a $13.36 Billion Future

Rising awareness, advanced imaging technologies, and aging populations are reshaping the global prostate cancer diagnostics landscape through 2033.

The global healthcare landscape is witnessing a transformative shift as prostate cancer diagnostics emerges as one of the fastest-growing segments within oncology. With increasing awareness, rapid technological advancements, and a growing elderly population, the market is poised for remarkable expansion in the coming years.

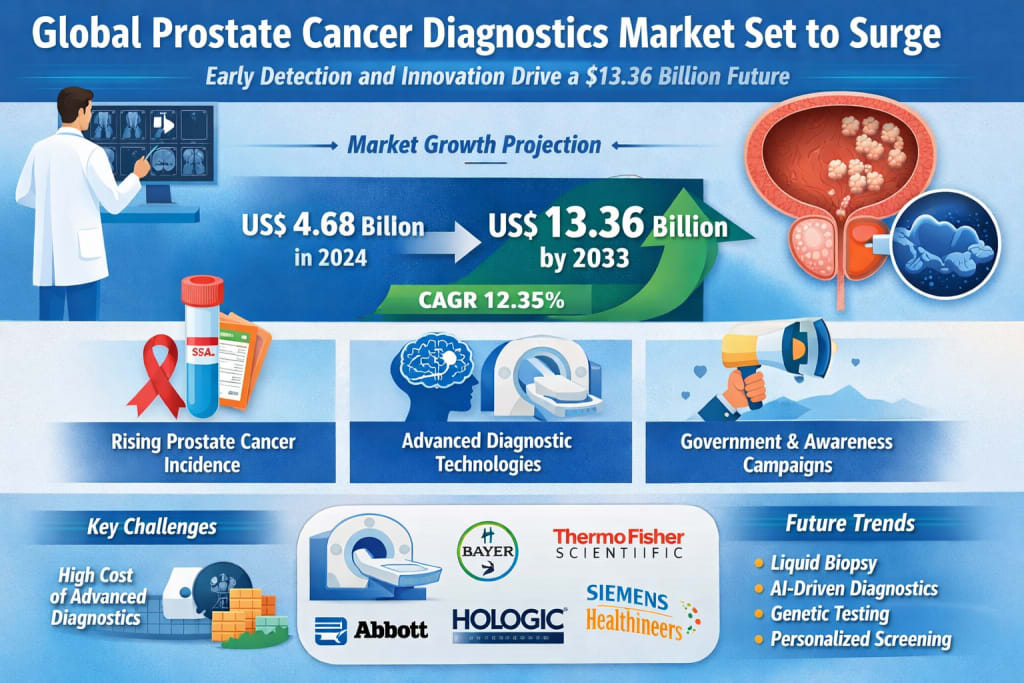

According to recent industry insights, the global prostate cancer diagnostics market is projected to grow from US$ 4.68 billion in 2024 to US$ 13.36 billion by 2033, registering an impressive compound annual growth rate (CAGR) of 12.35% between 2025 and 2033 . This growth reflects not only the rising prevalence of prostate cancer but also the increasing importance of early detection and personalized treatment strategies.

Understanding Prostate Cancer Diagnostics

Prostate cancer diagnostics involves a combination of clinical evaluations, laboratory testing, and imaging technologies aimed at detecting and assessing prostate cancer in men. The most widely used diagnostic methods include:

Prostate-Specific Antigen (PSA) blood test

Digital Rectal Examination (DRE)

Biopsy for tissue analysis

Imaging techniques such as MRI and ultrasound

Each of these tools plays a critical role in identifying abnormalities, determining cancer stages, and guiding treatment decisions. Early and accurate diagnosis is crucial, as it significantly improves survival rates and reduces complications.

Imaging technologies, particularly magnetic resonance imaging (MRI), have become increasingly important in recent years. These tools provide detailed insights into tumor size, location, and spread, enabling clinicians to adopt more targeted and effective treatment plans.

Key Drivers Fueling Market Growth

1. Rising Incidence of Prostate Cancer

One of the primary drivers of market expansion is the growing incidence of prostate cancer worldwide. The disease is now among the most commonly diagnosed cancers in men, with global statistics indicating that it ranks second only to lung cancer in prevalence.

Lifestyle changes, increased life expectancy, and genetic predispositions are contributing to the rising number of cases. As awareness grows, more men are opting for regular screenings, which directly boosts demand for diagnostic tools and services.

Early detection remains a cornerstone of effective treatment. As a result, healthcare systems are prioritizing screening programs to identify high-risk individuals at earlier stages.

2. Technological Advancements in Diagnostics

Technological innovation is reshaping the prostate cancer diagnostics market at an unprecedented pace. Modern diagnostic tools are becoming more accurate, less invasive, and increasingly efficient.

Key advancements include:

Multi-parametric MRI for enhanced imaging accuracy

PET scans for detecting metastasis

Molecular diagnostics and genetic testing

Artificial intelligence (AI)-based diagnostic systems

AI, in particular, is revolutionizing diagnostic workflows by reducing false positives and negatives. These systems can analyze biopsy samples and imaging data with remarkable precision, supporting clinicians in making faster and more reliable decisions.

Such innovations not only improve patient outcomes but also streamline healthcare processes, making diagnostics more accessible and efficient.

3. Government Initiatives and Awareness Campaigns

Governments and health organizations worldwide are actively promoting prostate cancer awareness and early detection. Public health campaigns, screening programs, and research funding are playing a vital role in expanding the market.

These initiatives encourage men to undergo routine screenings, leading to earlier diagnoses and better treatment outcomes. Increased funding for research is also driving the development of next-generation diagnostic tools.

As awareness continues to rise, the demand for diagnostic services is expected to grow steadily, particularly in emerging economies.

Challenges Hindering Market Expansion

Despite its promising growth trajectory, the prostate cancer diagnostics market faces several challenges.

High Cost of Advanced Diagnostic Technologies

Sophisticated diagnostic tools such as MRI and molecular imaging systems require significant investment in infrastructure, equipment, and training. This makes them less accessible in low- and middle-income countries.

The high cost of these technologies can also limit widespread screening, particularly among underserved populations.

Limited Access in Rural and Remote Areas

Healthcare disparities remain a major concern, especially in rural regions where access to advanced diagnostic facilities is limited. The lack of skilled professionals further complicates the situation.

These challenges often lead to delayed diagnoses and poorer outcomes, highlighting the need for improved healthcare infrastructure and outreach programs.

Segment Insights: A Closer Look

Benign Prostatic Hyperplasia (BPH) Diagnostics

BPH diagnostics focuses on detecting non-cancerous enlargement of the prostate, a common condition among aging men. Diagnostic methods include PSA testing, urinalysis, and imaging techniques.

Distinguishing BPH from prostate cancer is essential to avoid unnecessary treatments and ensure appropriate care.

Prostatic Adenocarcinoma Diagnostics

Prostatic adenocarcinoma is the most common type of prostate cancer and a major contributor to market growth. Diagnostic approaches include:

PSA testing

Biopsy

MRI and PET imaging

Genetic and molecular testing

Advancements in these areas are enabling more personalized treatment strategies, further driving market demand.

Preliminary vs. Confirmatory Tests

The diagnostic process typically begins with preliminary tests such as PSA and DRE. These are followed by confirmatory tests, including biopsies and advanced imaging, to establish a definitive diagnosis.

While preliminary tests are widely used due to their accessibility, confirmatory tests are essential for accurate staging and treatment planning.

End Users: Hospitals and Research Institutes

Hospitals remain the primary centers for prostate cancer diagnostics, offering comprehensive services ranging from screening to advanced imaging and biopsies.

Research institutes, on the other hand, play a crucial role in innovation. They are actively involved in developing new diagnostic tools, biomarkers, and technologies such as liquid biopsy and genetic profiling.

Collaboration between hospitals, research institutions, and biotech companies is accelerating the pace of innovation in this field.

Regional Market Highlights

Canada

Canada’s prostate cancer diagnostics market is growing steadily, driven by strong awareness and an aging population. The country’s healthcare system emphasizes early screening, ensuring widespread access to diagnostic services.

Germany

Germany stands out for its advanced healthcare infrastructure and adoption of cutting-edge diagnostic technologies. Techniques such as multi-parametric MRI and PSMA-PET/CT are enhancing diagnostic accuracy and improving patient outcomes.

China

China’s market is expanding rapidly due to its large population and increasing healthcare investments. Government initiatives and improved infrastructure are facilitating the adoption of advanced diagnostic technologies.

United Arab Emirates (UAE)

The UAE is witnessing significant growth in prostate cancer diagnostics, supported by government efforts to enhance healthcare quality and promote early detection. Innovations such as home-based PSA testing are gaining traction in the region.

Competitive Landscape

The global prostate cancer diagnostics market is highly competitive, with several major players driving innovation and expansion. Leading companies include:

F. Hoffmann-La Roche AG

Bayer AG

Thermo Fisher Scientific Inc.

Abbott Laboratories

Siemens Healthineers AG

Becton Dickinson and Company

Agilent Technologies Inc.

Hologic Inc.

Qiagen N.V.

OPKO Health Inc.

These companies are investing heavily in research and development, product innovation, and strategic collaborations to strengthen their market positions.

The Future of Prostate Cancer Diagnostics

The future of prostate cancer diagnostics lies in precision medicine and minimally invasive technologies. Emerging trends include:

Liquid biopsy for non-invasive cancer detection

AI-driven diagnostic platforms

Personalized screening programs

Integration of genetic and molecular data

These innovations are expected to transform the way prostate cancer is detected and treated, making diagnostics more accurate, accessible, and patient-centric.

As healthcare systems continue to evolve, the focus will shift toward early detection and preventive care, further driving market growth.

Final Thoughts

The global prostate cancer diagnostics market is entering a phase of rapid transformation, fueled by technological advancements, increasing awareness, and a growing need for early detection. With projections indicating a surge to US$ 13.36 billion by 2033, the market presents significant opportunities for stakeholders across the healthcare ecosystem .

However, addressing challenges such as high costs and limited access will be crucial to ensuring equitable healthcare outcomes. Bridging these gaps will require collaborative efforts from governments, healthcare providers, and industry leaders.

About the Creator

Australia Advertising Market Growth, Forecast, and Strategic Insights 2034

Advertising plays a critical role in shaping brand identity, influencing consumer behavior, and driving business growth. In Australia, the advertising industry has undergone a significant transformation over the past decade as businesses increasingly adopt digital channels, advanced analytics, and personalized marketing strategies. From traditional television and print media to digital platforms and influencer marketing, advertising continues to evolve alongside changing consumer habits.

By Rashi Sharma6 days ago in Trader

India Fertilizer Market Size and Forecast 2026–2034

India’s fertilizer industry is entering a period of steady growth as the country continues to strengthen its agricultural productivity to feed a rapidly growing population. Fertilizers play a vital role in ensuring higher crop yields, improving soil fertility, and supporting sustainable farming practices across the nation.

By Sakshi Sharma7 days ago in Trader

Comments

There are no comments for this story

Be the first to respond and start the conversation.