Solid Oxide Fuel Cell Market: Planar vs. Tubular Architecture Trends, Stack Scalability & Durability, & Industry Growth Outlook

The solid oxide fuel cell (SOFC) market is gaining momentum due to the growing demand for efficient and low-emission energy generation technologies.

According to IMARC Group's latest research publication, The global solid oxide fuel cell market size was valued at USD 1,642.5 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 4,545.9 Million by 2034, exhibiting a CAGR of 11.98% during 2026-2034.

How AI is Reshaping the Future of Solid Oxide Fuel Cell Market

- Predictive Performance Modeling and System Optimization: Machine learning algorithms analyze operating parameters like temperature, current density.

- Material Discovery and Electrolyte Design: AI-powered material science accelerates identification of high-performance perovskite catalysts.

- Real-Time Performance Monitoring and Fault Detection: Deep learning neural networks monitor voltage curves and operational data to predict polarization anomalies and equipment failures before breakdowns occur, enabling proactive maintenance scheduling and extending operational lifespans beyond 40,000 hours in commercial installations.

Solid Oxide Fuel Cell Industry Overview

Japan's comprehensive hydrogen strategy drives global SOFC deployment through substantial government support and industrial partnerships. The Ministry of Economy, Trade and Industry allocated JPY 170.8 Billion targeting a JPY 4 Trillion hydrogen market, with Honda receiving JPY 14.7 Billion and Toyota JPY 11.2 Billion to scale fuel cell production for commercial trucks. Honda's new Tochigi facility will produce 30,000 fuel cell systems annually by FY2028, targeting 5% market share in FC-powered trucks, rising to 30% by 2040.

Solid Oxide Fuel Cell Market Trends & Drivers

AI data centers are creating unprecedented demand for reliable baseload power solutions that bypass grid constraints. Bloom Energy secured agreements worth over USD 5 Billion, including a landmark 1 GW procurement with American Electric Power specifically for data centers, followed by a USD 5 Billion Brookfield partnership deploying SOFCs across global AI facilities. These deals dwarf typical installations, with single projects reaching 900 MW capacity in Wyoming. Oracle's deployment promises 90-day installation timelines, while Equinix expanded commitments beyond 100 MW across 19 facilities.

Government hydrogen initiatives are accelerating SOFC adoption through comprehensive policy frameworks and financial incentives. Japan's Hydrogen Society Promotion Act provides 15-year price support mechanisms for domestic and imported low-carbon hydrogen, complemented by JPY 3 Trillion in subsidies targeting commercialization across sectors.

Technological maturity and cost competitiveness are driving mainstream commercial adoption beyond pilot programs. SOFCs now match natural gas turbines on capital expenditure while consuming 15-20% less fuel and offering easier permitting through reduced emissions profiles. Installations achieving 13,000-hour operation demonstrate reliability, while advancements in lower-temperature operation reduce thermal stress and extend component lifespans.

Leading Companies Operating in the Global Solid Oxide Fuel Cell Industry

- Adaptive Energy LLC

- Aisin Seiki Co. Ltd.

- Bloom Energy

- Convion Ltd.

- Elcogen AS

- Fuji Electric Co. Ltd.

- Mitsubishi Heavy Industries Ltd.

- POSCO Energy

- SOLIDpower Group

- Sunfire GmbH

- Watt Fuel Cell Corporation

Solid Oxide Fuel Cell Market Report Segmentation

By Application:

- Portable

- Stationary

Stationary leads the market with around 80.3% of market share, driven by adaptability across residential, commercial, and industrial settings with combined heat-power cogeneration potential.

By End User:

- Commercial

- Data Centers

- Military and Defense

- Others

Commercial leads the market, offering cost-efficiency through high energy conversion efficiency, resilience to power outages, and fuel flexibility allowing businesses to select optimal fuel sources.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates with 38.7% market share, driven by abundant natural gas reserves, innovation hubs, federal Investment Tax Credits for fuel cells, and grid modernization initiatives.

Recent News and Developments in Solid Oxide Fuel Cell Market

- February 2026: Bloom Energy and Brookfield announced a USD 5 Billion partnership deploying SOFC technology across AI data centers worldwide, with the first European site expected before end of current period, creating new blueprint for powering AI-scale computing infrastructure.

- January 2025: Elcogen obtained EUR 5 Million investment from SmartCap venture capital fund backing Estonian Greentech firms, enhancing production capabilities for cost-efficient green hydrogen and zero-emission electricity through SOFC and SOEC technology.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About the Creator

sujeet. imarcgroup

With 2 years of hands-on experience at IMARC Group, I have conducted in-depth market research and analysis across diverse industries including technology, healthcare, agriculture, and consumer goods.

Keep reading

More stories from sujeet. imarcgroup and writers in Futurism and other communities.

Tablet Market: Healthcare Mobility Drivers, Antimicrobial Medical-Grade Tablets, & Industry Growth Outlook

According to IMARC Group's latest research publication, global tablet market size was valued at USD 84.6 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 202.4 Billion by 2033, exhibiting a CAGR of 9.67% from 2025-2033. Asia Pacific currently dominates the market, holding a market share of over 35.8% in 2024.

By sujeet. imarcgroup12 days ago in Futurism

How machines can learn from human behaviour

In order to understand where we are and where we are going, we need to understand where we were first. - Susan Fourtane Could a human behaviour simulator be embedded into a robot or online avatar to the point that it’s hard to distinguish between a real person or artificial intelligence? Scientists have been upping the stakes in this “Turing test” for years, to the point that human-mimicking programmes are ready to answer tricky questions, assist people with online shopping or be companions.

By Susan Fourtané 12 days ago in Futurism

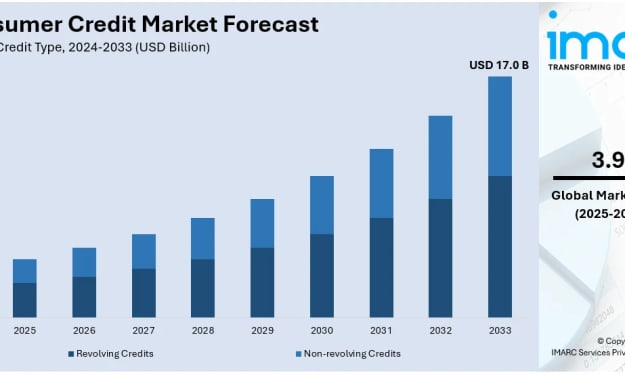

Consumer Credit Market Analysis: Personal Loans, Interest Rate Trends & Forecast to 2033

Consumer Credit Market IMARC Group – According to IMARC Group's latest research, the global consumer credit market was valued at USD 12.0 Billion in 2024. Looking forward, the market is projected to reach USD 17.0 Billion by 2033, expanding at a CAGR of 3.9% during 2025–2033. North America currently dominates the market, accounting for over 35% of the global share in 2024.

By Suhaira Yusuf4 days ago in Futurism

Comments

There are no comments for this story

Be the first to respond and start the conversation.