Drilling Fluids Market Encouraged Growth To USD 15.7 Billion by 2035 at 5.3% CAGR

The Global Drilling Fluids Market: Comprehensive Analysis and Outlook (2025–2035)

Overview

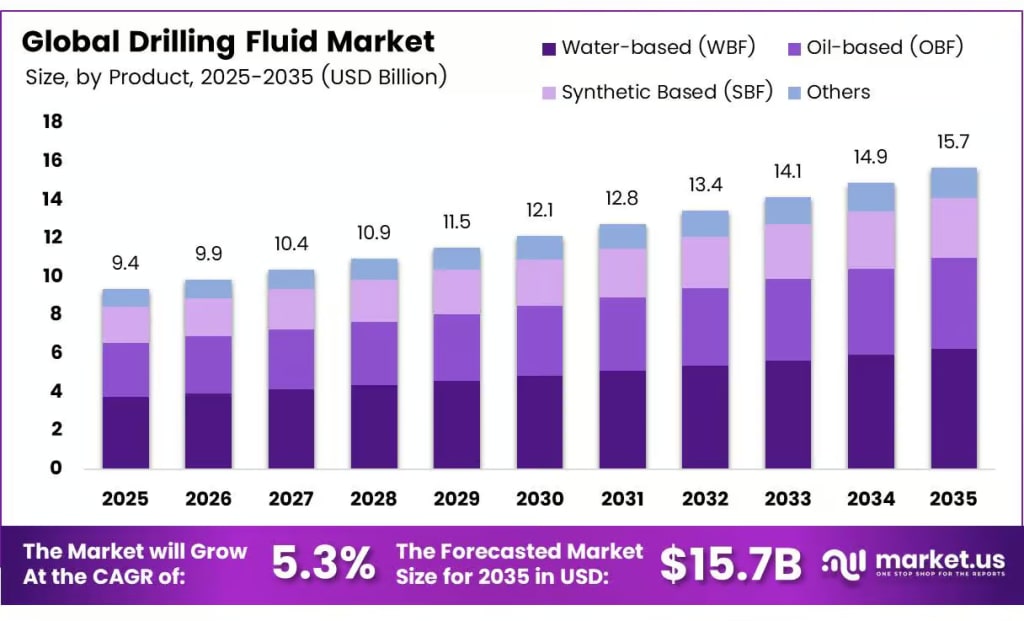

The Global Drilling Fluid Market size is expected to be worth around USD 15.7 billion by 2035 from USD 9.4 billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035. This growth aligns with sustained energy demand, shale and unconventional resource development, and the shift toward environmentally compliant fluids.

Drilling fluids (also known as drilling muds) are essential specialized fluids used in oil and gas well drilling. They cool and lubricate the drill bit, transport cuttings to the surface, and ensure wellbore stability under varying conditions. The market encompasses water-based, oil-based, and synthetic-based systems, deployed in both onshore and offshore settings to meet diverse geological and operational needs. Demand is driven by advancements in high-performance formulations for extreme pressures and temperatures in global exploration.

In the U.S., a key market driver, there were 918,481 producing oil and natural gas wells in 2024, with horizontal wells rising from 10% in 2014 to 22% in 2024. This underscores robust ongoing drilling activity requiring reliable fluid systems.

Key Takeaways

- The Global Drilling Fluid Market is valued at USD 9.4 billion in 2025 and is projected to reach USD 15.7 billion by 2035, at a CAGR of 5.3% during the forecast period 2026 to 2035.

- Water-based Fluids (WBF) dominate the market with a 52.5% share in 2025.

- Conventional wells lead the segment with a 78.2% market share in 2025.

- Onshore applications hold the largest share at 69.3% in 2025.

- North America dominates the regional market with a 38.1% share, valued at approximately USD 3.6 billion in 2025.

By Product Type

In 2025, water-based fluids (WBF) dominated the product segment with a 52.5% market share. These fluids are preferred for their cost-effectiveness, ease of treatment and disposal, and compliance with stricter environmental regulations. Their versatility suits onshore and shallow offshore operations, making them the primary choice for most global drilling programs. Oil-based and synthetic-based fluids serve more demanding environments but face greater regulatory scrutiny.

By Well Type

Conventional wells held a dominant 78.2% share in the well type segment in 2025. The industry continues to rely on a large inventory of vertical and deviated conventional wells in mature basins worldwide. These support steady demand through routine drilling, workovers, and maintenance, even as unconventional horizontal drilling grows in select regions.

By End-Use

Onshore applications led the end-use segment with a 69.3% share in 2025. Onshore drilling prevails due to extensive shale, tight oil, and conventional wells in North America, the Middle East, and Asia Pacific. Advantages include lower logistics costs, simpler fluid management, and higher overall consumption volumes compared to offshore.

Regional Insights

North America commands the largest regional share at 38.1% in 2025, valued at roughly USD 3.6 billion. The U.S. leads through massive shale and tight oil programs in basins like the Permian, Eagle Ford, and Bakken, bolstered by Canada's oil sands and unconventional gas. This positions North America as the top global consumer of drilling fluids.

Europe holds a moderate, stable position, centered on North Sea offshore activity (primarily UK and Norway). Declining onshore production in the EU, combined with stringent environmental rules, limits growth and favors synthetic and water-based systems compliant with offshore discharge standards.

Key players

- Baker Hughes, Inc.: A leader in oilfield technology, with strong drilling and completion fluids in its portfolio, benefiting from international demand.

- Halliburton, Inc.: Provides extensive expertise and global networks for onshore/offshore programs, investing in fluid innovation and digital tools to enhance wellbore quality and reduce costs.

- Newpark Resources, Inc.: Specializes in tailored water-, oil-, and synthetic-based fluids, focusing on technical differentiation, environmental compliance, and expansion in North America and select international markets.

- Schlumberger Ltd. (SLB): Achieves consistent growth (e.g., 10% YoY in recent periods) via robust international activity, well construction technologies, and AI/digital integration for optimized fluid management.

Conclusion

The global drilling fluids market is set for steady expansion through 2035, fueled by persistent oil and gas exploration, technological advancements in fluid formulations, and the need for efficient, environmentally responsible solutions. North America's dominance, water-based fluids' preference, and onshore focus form the core drivers, while key industry players continue to innovate amid regulatory and energy transition challenges. This positions the sector for sustained relevance in global energy production.

About the Creator

Hayden Kulas

I am blogger, digital marketing pro since 5 years and writes for Market.us. Computer Engineer by profession. I love to find new ideas that improve websites' SEO. He enjoys sharing knowledge and information about many topics.

Keep reading

More stories from Hayden Kulas and writers in Futurism and other communities.

Cellulose Esters Market Report: USD 24.9 Billion by 2034 at 5.8% CAGR

Overview The Global Cellulose Esters Market is on a strong growth trajectory, projected to reach USD 24.9 billion by 2035, up from USD 14.2 billion in 2025. This represents a steady compound annual growth rate (CAGR) of 5.8% throughout the forecast period (2026-2035). Cellulose esters are high-performance, bio-based polymers derived from natural cellulose.

By Hayden Kulas13 days ago in Futurism

How machines can learn from human behaviour

In order to understand where we are and where we are going, we need to understand where we were first. - Susan Fourtane Could a human behaviour simulator be embedded into a robot or online avatar to the point that it’s hard to distinguish between a real person or artificial intelligence? Scientists have been upping the stakes in this “Turing test” for years, to the point that human-mimicking programmes are ready to answer tricky questions, assist people with online shopping or be companions.

By Susan Fourtané 12 days ago in Futurism

Watching The End Of The World From The Diner

Introduction I am not sure how to approach this. Guy Peellaert was an amazing artist who created iconic fantasy images of famous people, usually musicians or politicians, as well as creating commissioned album covers such as "It's Only Rock'n'Roll" by The Rolling Stones and David Bowie's "Diamond Dogs" which you can read more about below.

By Mike Singleton 💜 Mikeydred 3 days ago in Art

Comments

There are no comments for this story

Be the first to respond and start the conversation.